In recent years, increasing pressure to control costs whilst ensuring the highest quality of care is delivered to patients, has led to the increased consolidation and integration of hospitals into groups or multi-hospital networks and systems. This is in part due to changes in the reimbursement system such as the Affordable Care Act (2011) that emphasise patient outcome and quality of care.

By reorganising themselves into bigger groups, hospitals can drive improvements in efficiency, care quality, coordination and costs. Although these changes can positively impact care delivery, they may create challenges for medical device manufacturers through the exertion of greater negotiating power and price commanding. In order to succeed in this changing market, medical device firms must have a good understanding of the current landscape (to optimise commercial strategy) and what they can do to ensure new products and services align to the changing needs of health systems, which can be done with the help of an international healthcare consultancy.

Organisation and delivery of care across health systems

The purpose of an Integrated Delivery Network is to deliver more organised care within a contained healthcare ecosystem. There are two types of organisational structure:

- Health systems are organisations that bring together people, institutions and resources to deliver health services to large patient populations. To be classed as a health system it is typical for these organisations to include at least one hospital, one group of physicians, and be connected through a common ownership/joint management structure.

- Health networks on the other hand can be composed of a group of hospitals, physicians, insurers and/or community agencies all working together to deliver and coordinate care services for the community.

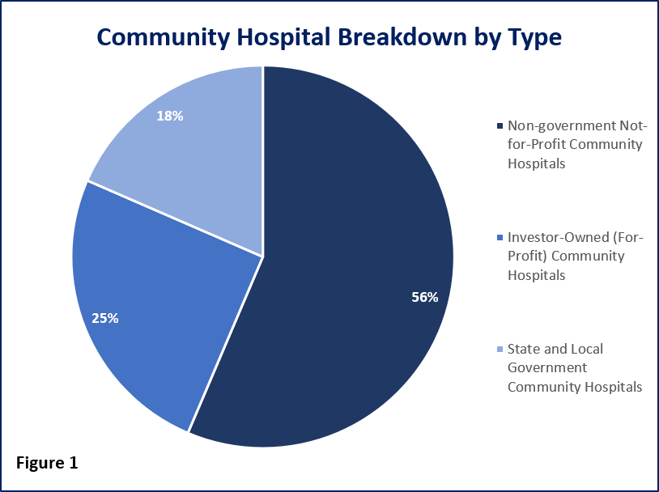

Figure 1. Graph shows a breakdown of the type of community hospitals within the US

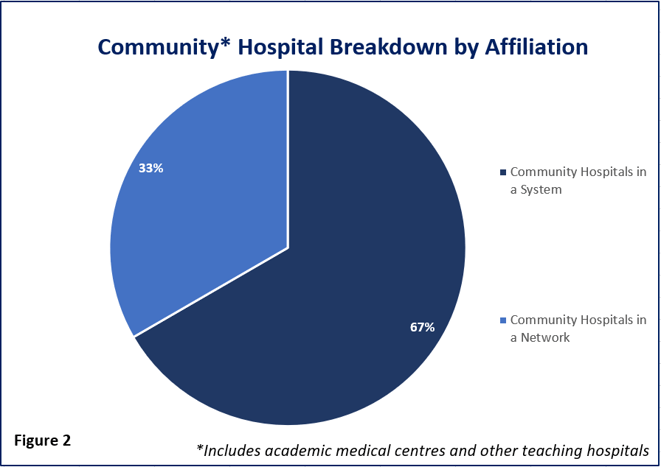

Figure 2. Graph shows the affiliation of community hospitals within the US, a majority being part of a health system

Recent trends have led to an increased consolidation of hospitals into networks

Consolidation of healthcare facilities into delivery systems has occurred at a fast pace within the United States. This has consisted of small, independent practices shifting to larger more unified organisations. While the drivers that are leading to health system consolidation are more evident (for example increasing pressure and reduced growth in hospital reimbursement) evidence of the benefits of integration are limited. Some of the perceived benefits are:

- An ability to leverage economies of scale and scope

- Continuous reduction or duplication of resources

- Increased market influence and provision of quality services

- More standardised and impactful training of physicians and hospital staff

Figure 3. The organization of a typical Clinically Integrated Delivery Network; these consist of multiple health facilities that are part of a single group and typically have shared governance, clinical programs, care management, contracting and infrastructure

At a higher level, IDN’s may also be part of Group Purchasing Organisations (GPOs). These are alliances that help healthcare providers realise cost savings and efficiencies when purchasing from various suppliers. While GPOs do not own IDN’s, membership allows for:

- Negotiating better prices for products and services by leveraging joint negotiation

- Evaluating products and services to achieve maximum therapeutic value and guaranteed patient safety

- Offering benchmarking and control opportunities to drive health system efficiencies in the long-term

Ensuring your medical technology innovation is reimbursed and adopted across all health systems

Prior to being able to sell a new medical technology in a care setting, it must first be approved by the Food & Drug Administration (FDA). Upon successful revision, the approved device receives market authorisation meaning it can be sold. Reimbursement, however, is a very different matter; in fact not only does a device have to fall under a specific reimbursement code (e.g. CPT, ICD, DRG) it must also undergo a coverage review that assesses the possible benefits of the product before it is paid for by public or private payers.

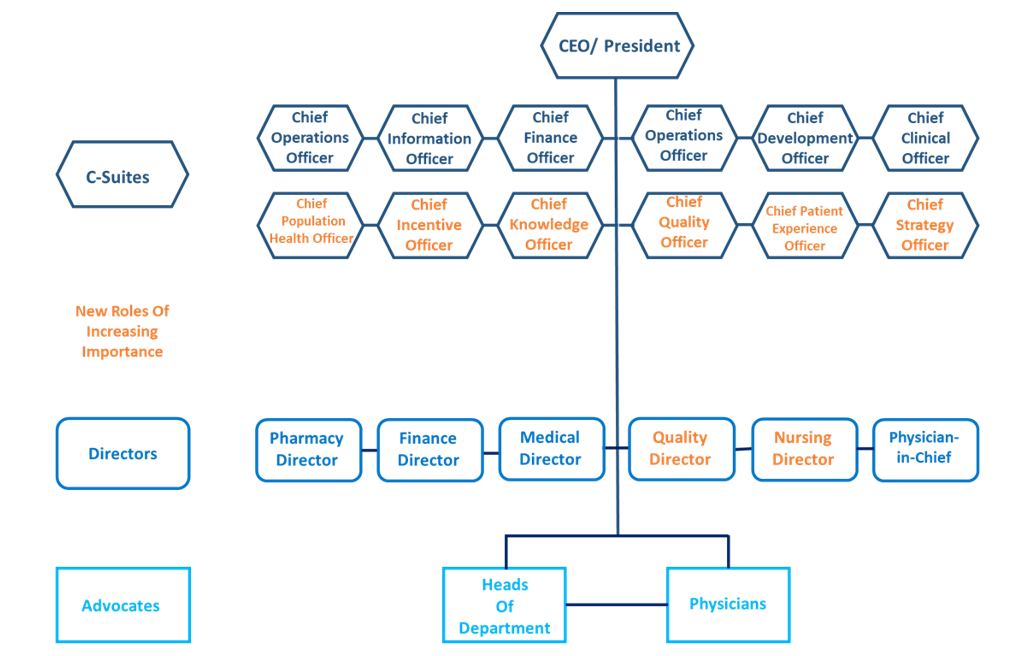

If you are considering engaging with an IDN it is important to understand how these systems are structured and who the key stakeholders are, which is outlined in Figure 4. These roles are evolving to accommodate for organisational changes with a greater emphasis on patient care and outcome. It is crucial to consider the stakeholders and their incentives; doing so will help promote the value of a new product within an IDN and optimise commercial strategy for success in this evolving landscape.

Figure 4. This figure represents a typical structure of an integrated delivery network, with the main decision makers having been arranged into three groups: C-Suites, Directors and Advocates.

- Although C-Suites are not directly involved in deciding which products are prescribed or will be part of the hospital formulary, they may influence product access and utilization or system structure/ organization. These roles have adapted to include positions focussed on performance and reimbursement. C-suites are likely to respond well to a product which aligns with their system goals and shows benefits for profit, health and performance.

- Directors includes Clinical and Pharmacy leaders that are part of the Value Analysis committee. Often make key inclusion and exclusion product decisions based on best clinical outcome and economic suitability. Gaining support from these directors is key as they ultimately decide the value of a product and communicate with the C-suite on its appropriateness for the system.

- Hospital clinicians typically fall under the Advocates group. Across most IDNs, endorsement by clinician advocates is essential to ensure inclusion of a product into an IDN’s formulary. Advocates have the capacity to endorse the product throughout an organisation if they believe it is beneficial for patient.

With the ever-changing IDN landscape and an increasing consolidation of hospitals into larger groups, stakeholder roles will continue to evolve. As such, engaging with these stakeholders and understanding their decision-making processes will become an even more essential aspect for ensuring product success. As an international healthcare consultancy, conducting market research with these groups allows medical device manufacturers to understand what priorities health systems have, their product/service needs, and the direction in which they are moving in. Accessing insights in this manner will undoubtedly lead to increased uptake and market share for products that can demonstrate an added benefit.

IDR Medical recognises the need to ensure your medical technology demonstrates value to clinical advocates, administrative stakeholders, and payers. As experts in medical market research, we can help your firm demonstrate the added value of your innovative solutions to ensure adoption and reimbursement.

If you would like an initial telephone discussion, or a face to face meeting to understand how we can help your device take market share, please contact us here.